With the rapid penetration of technology into all spheres of life, from ordering food at home and calling a taxi to walking dogs and renting cars, online marketplaces are becoming the primary type of commerce between the buyers and sellers of goods and services. Russia is gradually building a pool of popular digital platforms for eCommerce, including foreign marketplaces such as AliExpress (China) and Amazon (US) and a variety of Russian ones. The biggest and most popular Russian websites are Wildberries, Ozon, and Lamoda.

A modern marketplace

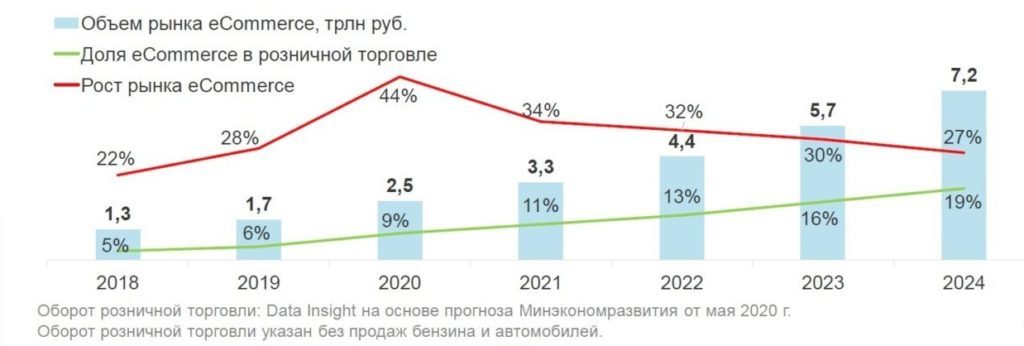

According to the Data Insight analytical team, by 2024, eCommerce will account for 19% (RUR 7.2 trillion) of all retail sales in Russia. At the end of May 2020, the same indicator was at the 9% (RUR 2.5 trillion) level.

Major online stores’ and marketplaces’ investments in advertising to attract new customers, expanding their geography of presence and delivery options, as well as the months of coronavirus lockdown and self-isolation have provoked a rapid growth of the eCommerce market. In the first half of 2020, online sales of FMCG products grew 4.3 times compared to the same period in 2019.

According to experts, the ‘non-working days’ introduced to prevent the spread of COVID-19 last year have brought at least 10 million Russians into online commerce; there is no doubt that this figure will grow. In the current paradigm of the growing digital economy and globalization, as well as modern technologies’ penetration into various spheres of our lives, we can confidently talk about the limitless potential of using online commerce platforms for development of entrepreneurship.

There are several industries that have already embraced the marketplace concept — property rentals, travel, housing and utilities, delivery of ready-made food and groceries, car rentals and purchase, education, healthcare, employment and many others. Incidentally, they constitute a basic set of services that is crucial for society.

But it’s time to ask ourselves — what will happen at the next stage of integration?

One of the obvious further extensions for online commerce is certainly financial technology. Even now, there is a demand for such technology and multi-brand ecosystems that would offer goods such as bank cards and credit products, insurance services, full-cycle customer service and financial consulting, mobile banking, investment products, services for opening and managing brokerage accounts, IIS and much more.

Marketplace: A new life for financial markets

As stated earlier, we are seeing an inevitable global integration of marketplace technology into many areas of our daily lives. Due to the fast growth of financial markets, the application of technology in retail banking and financial products (loans, debit cards, insurance services, investment products and related services) is becoming more and more popular. The Marketplace project, initiated by the Bank of Russia in December 2017, immediately comes to mind. The goal of the project is to create a legislative and regulatory framework for remote retail of financial products across Russia, bypassing geographical restrictions, with legally relevant information on transactions performed via financial platforms subsequently stored in a special register — the Financial Transaction Registrar (FTR). The State Duma, the Russian parliament’s lower house, passed the bill on the system in the summer of 2020, actually creating a legislative framework and new opportunities for its further development based on market principles.

Finuslugi.ru (“Financial services”), a new project of the Moscow Stock Exchange that became the first financial “supermarket” created under the new law on Central Bank electronic platforms, is one project worth mentioning. The platform currently offers such services as comparing deposit options from several Russian banks. Users can also buy a compulsory motor insurance (OSAGO) on the website.

Also in April 2020, the Real Estate Developer Account on Sberbank Business Online added a new service integrated with a marketplace for developers. The platform helps with searching for management companies or co-investors when applying for project financing. Developers can apply for real estate project lending, monitor the processing of their applications and submit any supporting documents required.

All the other digital platforms on the market can only be defined as marketplaces very loosely: the well-known banki.ru, sravni.ru, vbr.ru and others are more like multi-brand shop windows. They do not have a platform structure and basically post offers available on the market without any additional services. Essentially, they are major lead generators with significant advertising budgets.

What about the West?

Historically, the marketplace technology is better developed in the West and, as it is often the case, best Western trends are slowly but surely finding their logical extension in Russian reality. But it should be noted though that Western fintech is pursuing a completely different path. Most digital platforms in America, Europe and Asia are extensively using the P2P lending model. P2P lending means that an investor can provide a loan to an individual or a business via a special online service (a peer-to-peer platform). This service acts as a mediator that establishes rules of the game for users and helps them find each other.

There are plenty of Western cases that deserve a mention. For example, CommonBond (USA) is a marketplace where students and recent graduates can refinance their student loans. The project was launched in November 2021 and since then, more than 100K students have been issued loans worth over $2.5 bio in total.

Another project is Upstart Loans (USA), a universal P2P lending platform where one can get a loan for anything, from studies to business. Customers follow three simple steps to get a loan: they sign up, select a loan term and set up a loan payment schedule.

The world’s first P2P lender was Zopa (UK) founded back in 2004. Its name being an acronym for “a zone of possible agreement,” the platform now has over 45K active investors and 71K borrowers meaning it continues to grow even so many years later.

Then, there is LendInvest (UK), a P2P lender specializing in real estate. On its home page, you can choose if you want to be a borrower or an investor. Since its launch in 2008, the company has issued £1.5 bio ($1.9 bio) worth of loans for purchasing, building or maintaining one’s property. Moreover, the company’s founders and employees remain its majority owners. On August 10, 2017, LendInvest successfully had its retail bonds listed on the London Stock Exchange.

SMAVA (Germany) is a German marketplace for comparing private loans. Its database includes loans by different banks as well as proprietary loan offers and loans from private creditors. SMAVA will pick the best loans and only those that the customer can pay back. To find a perfect match, one should state the purpose of the loan, the amount (from €1 to €120K) and the term.

Jimubox (China) is a popular financial marketplace in China and one of the first fintech companies working with Chinese banks and licensed to operate online. The startup is also a member of the National Internet Finance Association of China and the Beijing P2P Association. The biggest deal of the service is that it is tailored for investors and those who want to become investors. Jimubox helps create a “perfect” portfolio for every investor by researching their interests and risk-taking levels. It is also possible take out a private or business loan via Jimubox.

The benefits of financial marketplaces

The first and most obvious advantage is the user’s ability to receive the necessary financial services in a one-stop-shop. For instance, to receive a loan or a credit card, the client fills in the form on the website in just two clicks, goes through an identification process, and then receives the bank’s decision and the product online. If one of the banks rejects the loan application, it does not mean that the others will do the same. Another undeniable advantage of the technology is the opportunity to compare proposals and pick a product that meets the user’s requirements.

It is noteworthy that a marketplace by its nature entails a higher level of competition between service providers because the terms of competitive proposals are available to everyone: it can be seen at the examples of Wildberries, Ozon, Yandex.Market. The pricing policy and conditions of rival companies are open, which helps understand why a product is a slow mover even if it has the same properties as the others. This leads to an increased level of competition, but most importantly, product proposals for the user are getting better. The technology also allows suppliers to solve a series of problems, including logistics. There are the issues of ‘last mile’ and communication with the client at the final stages of the logistics chain. Many banks and insurance companies cannot sell their products in other regions because they lack resources, and thus are limited in markets, although the service “a 10% APR loan” is the same in Moscow and in, say, Ussuriysk. There is no difference whatsoever, therefore financial marketplaces will develop like product marketplaces. And we know well how the latter are doing: AliExpress has spread worldwide, Ozon has successfully launched an IPO and Yandex.Market is quite popular in Russia. By the way, another weighty argument in favor of the technology is that according to the current law, each registered marketplace has to join a financial transaction system, the Financial Transaction Registrar. While purchasing a product or a service, the information on the performed transaction is instantly sent to the Central Bank, which guarantees its validity and legitimacy and confirms that the transaction was implemented legally, with consideration of all consumer interests; this will positively affect the market’s general transparency and openness.

Conclusion

We could endlessly talk about development of the technology and cite typical examples; yet, in fact, we have to understand that marketplaces are the most dynamically developing format of commerce in Russia that opens fundamentally new opportunities for the business sector. Today, most consumers seek to actively use digital services and buy products and services online. The marketplace technology is flexible to adapt to new products and services, as well as to citizens’ lifestyles and customer behavior. Initially, marketplaces served to help sellers and customers find each other; eventually, these platforms have shifted their development vector towards the end buyer and started offering an additional set of essential services. Marketplaces have grown into a multifunctional full-cycle service that allows handling consumers’ specific problems and needs, and provides new opportunities to businesses and suppliers of financial products and services, which has become particularly evident amidst the global lockdown.

According to the Dealroom research team, the COVID-19 crisis served as a growth driver for 55% of marketplaces and provided new opportunities for their adaptation and growth; another 23% of companies faced a slump in consumer activity — yet they are expected to quickly restore to the pre-crisis levels within a short period of time following the lifting of the lockdown as they operate in prospective sectors. Consequently, a total of 78% of all companies could expect more or less promising future.

This year is expected to be more challenging for the banking sector than the previous one — not only due to the epidemiologic situation but also to the fall in interest rates, which has slumped to a record low. This means that boosting product sales will be vitally important for banks, with their activity to increase client base only to grow. However, not all banks will be able to do so as there is marketing of major players in the retail market which will be increasingly dominant.

Therefore, we can note an obvious relevance of financial marketplaces for small and medium businesses; the former help solve a whole scope of issues, including those related to the logistic chain, communication with customers during all stages of transaction, and distribution problems. The integration of the marketplace technology is definitely at its initial stage; yet, the crisis is providing new opportunities, and we can already confidently say that despite the pandemic and the economic instability we will see active development of the market in general as well as specific fintech projects in particular. This has been proved by creation of an effective legislative framework.

Russia is currently walking the path of the sector’s consistent development through increasing positive competition, improving quality of financial products for businesses and consumers, and boosting financial culture of consumption of loan products, which is an essential part of the national economy’s growth.

We should particularly note a “Russian scenario” for development of financial marketplaces through active support by Russia’s Central Bank. Hopefully, the state regulator’s involvement will allow for a greater availability of financial services for a large amount of population regardless of geographical location, and for increasing effective competition in the market through technological support for small and medium-sized banks as well as insurance companies at the regional level.

By Mikhail Yefremov

Director General, Finfort Group